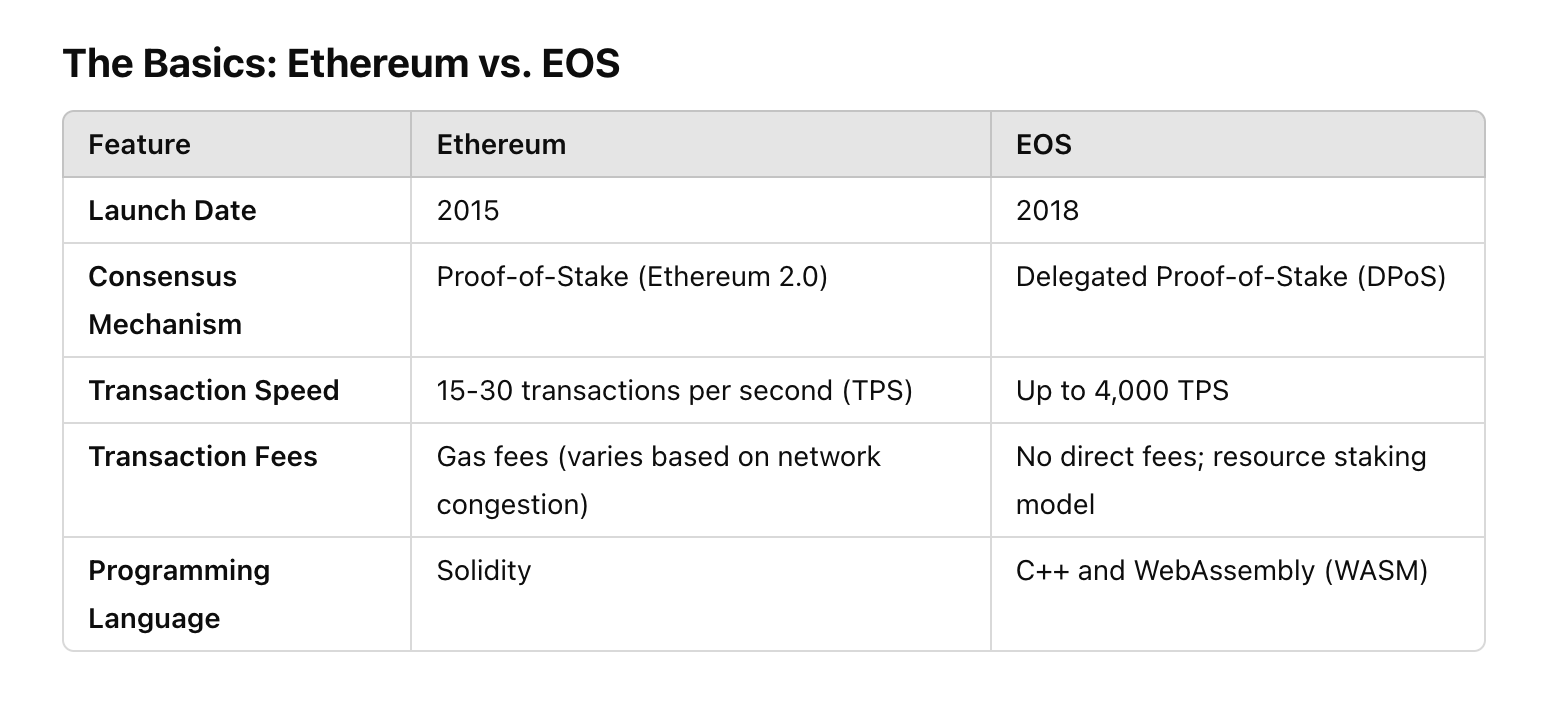

EOS vs Ethereum: The Battle of Blockchain Titans

How to Lease Cryptocurrency: A Step-by-Step Guide

Imagine a world where digital cats are so popular they bring a revolutionary blockchain to its knees. Sounds absurd, right? Well, welcome to the universe of CryptoKitties, the pioneering blockchain-based game that not only created waves in the world of collectibles but also highlighted the scalability challenges of Ethereum. Let’s explore how these virtual furballs reshaped blockchain gaming, their highs, lows, and their lasting impact on the crypto ecosystem.

#CryptoKitties

#BlockchainGaming

#NFTs

#Ethereum

#DapperLabs

#DecentralizedApplications

#DigitalOwnership

#BlockchainTechnology

#NonFungibleTokens

#NFTCollectibles

#GamingOnEthereum

#CryptoGaming

#BlockchainInnovation

#EthereumSmartContracts

#NFTMarketplace

In the ever-evolving landscape of blockchain technology, Waves Blockchain has carved a niche for itself as a user-friendly, scalable, and innovative platform. Since its inception in 2016, Waves has steadily gained recognition for its unique approach to decentralization, seamless token creation, and robust ecosystem of tools designed to empower individuals and businesses.#WavesBlockchain #BlockchainTechnology #CryptoInnovation #DecentralizedFinance #DeFi #CustomTokens #LPoS #CryptoEcosystem #SmartContracts #WavesDEX #BlockchainSimplified #NFTsOnWaves #CrowdfundingCrypto #SustainableBlockchain #CryptoForBusiness #WavesCommunity #FutureOfFinance #Tokenization #CryptoForEveryone #BlockchainMadeEasy

The Ultimate Guide to PoW and PoS Coins

Understanding the Types of Stock Options: ISOs vs. NSOs

Dive into the fascinating world of meme coins and crypto whales! Learn how viral cryptocurrencies like Dogecoin and Shiba Inu gain popularity, and discover the role of whales—those major market players who hold massive amounts of crypto and influence price movements. Whether you're a crypto enthusiast or a curious beginner, this post breaks down the buzz and offers tips for navigating the hype.

**Post Tags:**

#Cryptocurrency #MemeCoins #CryptoWhales #Dogecoin #ShibaInu #CryptoInvesting #Blockchain #CryptoMarket #Altcoins #CryptoTrading

The new season is a great reason to make and keep resolutions. Whether it’s eating right or cleaning out the garage, here are some tips for making and keeping resolutions.

Day trading is a dynamic and fast-paced strategy that allows traders to capitalize on intraday market movements. Discover the tools, strategies, and mindset required to succeed in day trading, from mastering technical analysis to effective risk management. Whether you’re a beginner or looking to refine your skills, this blog post provides actionable insights to help you thrive.

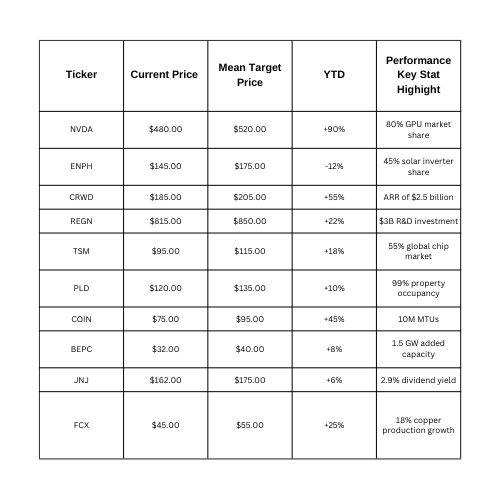

Top Investments for 2025 - Stock

Discover the top 5 stocks poised for growth in 2025: NVIDIA, Enphase Energy, CrowdStrike, TSM, and Freeport-McMoRan. From AI innovation and clean energy to cybersecurity and essential materials, these companies lead the way in shaping tomorrow’s markets. Explore why they’re worth your portfolio consideration!